Markets and commentators alike are fixated on inflation, as signs suggest it is coming and will be anything but transitory.

Meanwhile, most central banks – including the Reserve Bank of Australia – are of the view that any up-tick in inflation will only be temporary. The bond market, however, has already begun to price in an increase in inflation, with the US 10-year Treasury yield rising 68bp to 1.59% for the calendar year to 9 May and the Australian 10-year bond yield rising 65bp to 1.63%.

Warren Buffet made the following comments regarding inflation at the recent Berkshire Hathaway AGM: “We’re seeing very substantial inflation. It’s very interesting. We’re raising prices. People are raising prices to us, and it’s being accepted …. we really do a lot of housing. The costs are just up, up, up. Steel costs, just every day they’re going up … So it’s an economy really, it’s red hot. And we weren’t expecting it.”

Just as Warren Buffett didn’t expect to see inflation, we don’t believe consumers are expecting it either. Inflation expectations have fallen significantly since the GFC, but the winds of change are here.

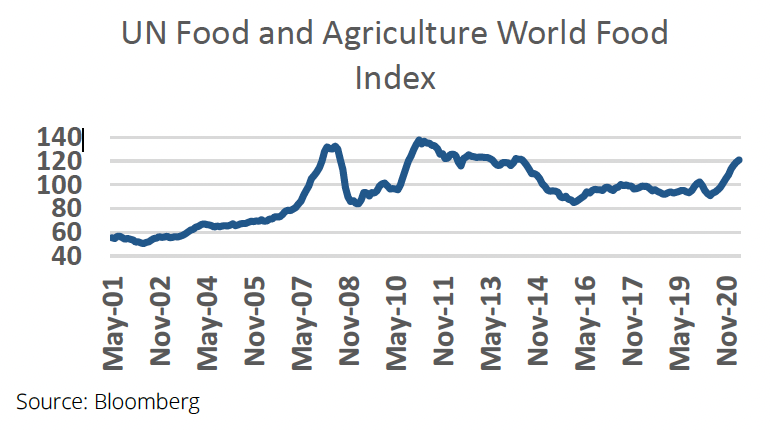

Food is perhaps the most obvious commodity where inflation will be quickly noticed by consumers; and this could be soon, if a recent report by the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) is to be believed. ABARES believes the price of a range of fruit and vegetables could rise between 7-29% due to a drop in supply caused by the COVID-induced absence of Australia’s traditional “backpacker fruit pickers”. The Food and Agriculture Organization of the United Nations Food Price Index, which tracks monthly changes in the international prices of commonly-traded food commodities (including meat, dairy, cereals, vegetable oils and sugar) is up 30% year on year and has risen for ten consecutive months. This will have quite an impact on the purchasing power of consumers, particularly in third world countries.

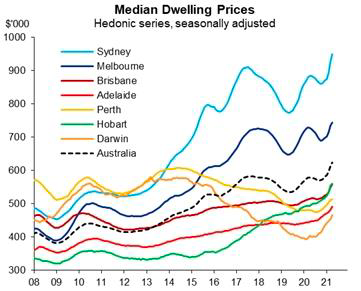

There are certain parallels between the economic and political backdrop of today and that of the 1970s. Housing and commodities were two of the few asset classes that acted as effective inflation hedges then, and we suspect they will similarly perform strongly today. Right now, with inflation rising, borrowing costs reasonable and the supply of homes quite low in some Australian states, the stage is set for homes to once again become an inflation hedge. The housing market in the US and Australia has leapt, and we believe is still in the early stages of this rally.

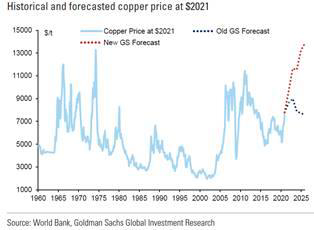

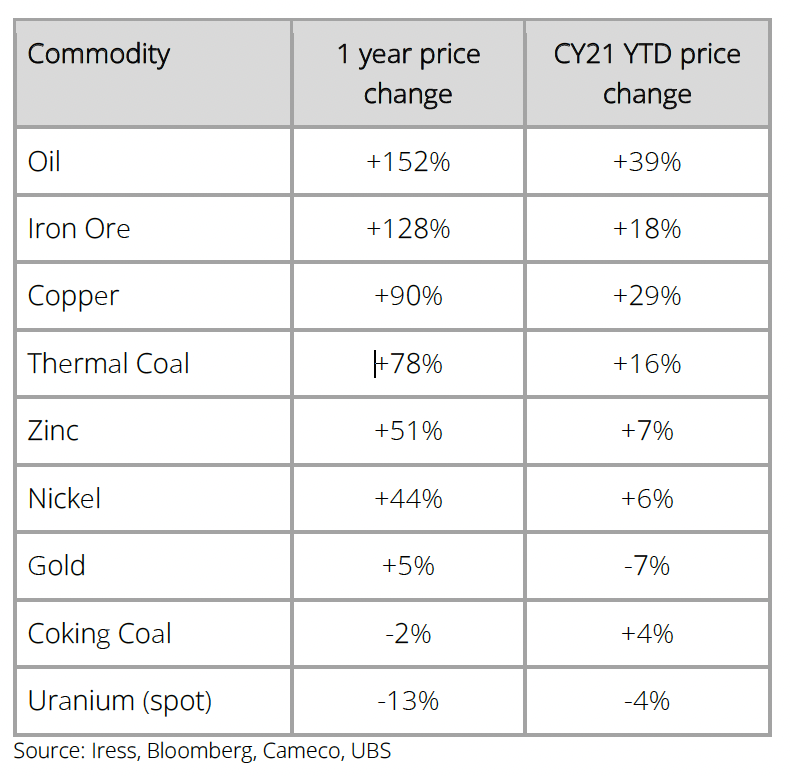

Meanwhile, over the past year the copper price has risen 90% to US$4.47/lb, benefiting from strong demand (as government and central bank stimulus drive a recovery in global growth) and weak supply (due to years of underinvestment). With a tight market and a very low starting point for inventories, we believe the copper bull market has further to run. Indeed, Goldman Sachs believes that copper’s critical role in decarbonisation will force the price to US$15,000/t (US$6.80/lb) by 2025 – 50% higher than the current price. According to Bloomberg, Glencore’s CEO echoed those thoughts recently, suggesting a US$15,000 price is required to incentivise new copper projects.

Copper is not the only commodity that is seeing strong price growth, as can be seen from the table below.

Looking more short term, Friday’s US payroll report showed 266,000 new jobs were created against market expectations of around 1 million. But what piqued our interest was the rally in the US market that ensued after the release, with the market simply shrugging off the poor economic news. The conclusion to draw is that weaker employment growth will motivate the US Federal Reserve to extend stimulus and maintain a lower for longer interest rate setting, giving the equity market plenty to cheer about.

We believe higher inflation and higher global debt are here to stay. But the day of reckoning is still some way off..

Equity Trustees Limited (“Equity Trustees”) (ABN 46 004 031 298), AFSL 240975, is the Responsible Entity for the Kardinia Long Short Fund (“the Fund”). Equity Trustees is a subsidiary of EQT Holdings Limited (ABN 22 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX: EQT).

This publication has been prepared by Kardinia Capital Pty Ltd to provide you with general information only. In preparing this information, we did not take into account the investment objectives, financial situation or particular needs of any particular person. It is not intended to take the place of professional advice and you should not take action on specific issues in reliance on this information. Neither Kardinia Capital Pty Ltd, Equity Trustees nor any of its related parties, their employees or directors, provide and warranty of accuracy or reliability in relation to such information or accepts any liability to any person who relies on it. Past performance should not be taken as an indicator of future performance. You should obtain a copy of the Product Disclosure Statement before making a decision about whether to invest in this product.